Alan Dustin is seasoned financial advisor who has spent twenty-five years guiding Canadian investors to financial success. Alan graduated from the University of Waterloo in 1990. Before becoming a financial advisor, he was an options specialist for one of Canada’s leading discount brokerages. He has appeared as an expert commentator on CBC and CP24, and has published numerous articles for the Investor’s Digest of Canada and Canadian MoneySaver. He lives in Toronto. This interview took place at Toronto Reference Library on January 25, 2018 (Thursday @ 1200). The duration of the interview was 33 minutes and 51 seconds.

Urgen Kuyee: Hi Alan, why don’t you let my readers know a little bit about yourself and how did you get into personal finance?

Alan Dustin: Sure. I have been a financial advisor for about 25 years. Originally, my career was in a different direction. I was really in the trade profession and right now we’re in the middle of winter here in Toronto, it’s been very cold the last few weeks. When I was working, it was apprentice electrician. In my apprenticeship, I was working outside on buildings being built that had no sort of structure yet. So, I was outside and on very very cold days. I decided one day when I was assigned to work in a brokerage firm on their trading floor. When I was on the trading floor, I observed as I was working and I was running wires for their computer systems, I observed these guys yelling and screaming at each other and it was that day that I really got hooked. That was the day I said maybe I am destined for greater things. So, it was the pain of being on a skyscraper in downtown Toronto in the middle of winter with no windows and trying to stay warm with the fact that, that day on a trading floor, I knew right away what I wanted to do.

UK: How many years ago was this?

AD: That was in the mid 80’s.

UK: What is the best thing about working as a financial advisor? What are some of the challenges?

AD: Hahaha. The best thing is it’s incredibly rewarding. Some of the challenges are that it’s very difficult to stay positive all the time. So, there is lot of time you have to deal with people’s emotions and their psychology and that goes along with the market as well.

UK: Big time.

AD: That’s a challenge. Another challenge is rejection and I would say that for any sales professional. You have to deal with rejection on a daily basis and you have to do things personally to develop in order to sort of overcome that negativity that you experience with getting a lot of no’s. But, the yeses are very rewarding.

UK: What are one to three books that have greatly influenced your life?

AD: That’s an excellent question. Okay, it’s funny because someone just asked me this question a few days ago. There are a number of books and I’ll give them to you, one at a time. I have always been interested in markets even before I even got into the profession. When I was in my teens, I will go back to my childhood and everyone has his or her story in life. I saw that investing or making money in the market was a way for me to break out of my middle class family shall we say. And, I always knew there was something that I would be able to do that was great myself and then hopefully share that or be able to do that for other people.

It’s been in my DNA for a very long time that I knew that this was something I wanted to do. It was not as clear as it is today as it was back then. But a couple of books that really influenced me are these, there is a series by Jack Schwager called the Market Wizards, the new Market Wizards, hedge fund Market Wizards. What he does is he’s done exactly what you have done. He has interviewed people that have been incredibly successful. We are talking billionaires, people that have made incredible amount of money in the market and psychology and the trials and tribulations that they have gone through. So, that’s probably my favourite book. And, that’s what has really inspired me to try and do what I’m doing today by reading about other people that have had the same challenges. I like success stories, I like how people risen from mediocrity to ultimate, you know amazing success.

There was a book I read about 10 years ago. It was titled How to Make Money in Stocks by William J O’Neil. He is the founder and publisher of the investors business daily. That book was really, I didn’t copy it, my book is not a copy of his book but it is along the same theme. There is a blue print, a method or a strategy to employ in order to be successful in the stock market, investing in stocks. I formulated a lot of ideas in my book from his book.

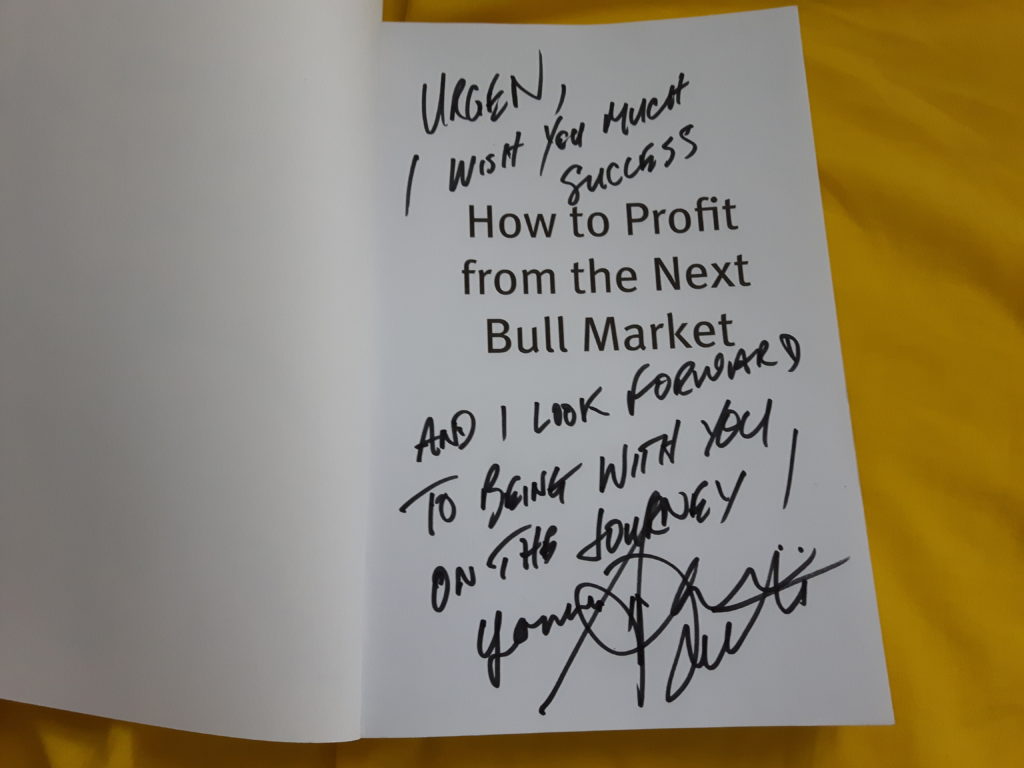

UK: Let’s talk about your book. “How to Profit from the Next Bull Market”. What led you to write this book?

AD: Well, in this industry you have to be prepared to go through a number of transitions. So, downsize, upsize, whatever you want to call it. This business has seen the ups and downs and that’s the part of being in the financial industry. It is just the part of the business that you constantly move, whether it’s your decision or company’s decision to move on. Back in the 2009, which was the bottom of the last market, I found myself out of work from being downsized. I found a job at a credit union and I was almost there for, let’s say 7 years. And, then I found myself downsized again. Then, I decided that perhaps it’s time for me to get back and build my own business, my own book of business again back in the financial industry as a full commission advisor and that way my destiny would be determined by one person and one person only, that is myself. And, one way to differentiate myself would be ultimately to write the book.

UK: How long did it take you to write this book?

AD: It took about a year.

UK: Every investor knows that the bulk of investment returns are made in a bull market. We are in the 9th year of a bull market. In your latest blog, you have quoted, Warren Buffett “A bull market is like sex. It feels great just before it ends”. Is it fair to say that most of the gains have already been made? Both of us know a bear market is approaching.

AD: Yes, I would say it is fair to say that most of the gains have already been made. In fact, here’s what people don’t really understand. People think that markets are based on logic and strategy and fundamentals but they have nothing to do with that. Markets are based on emotions and psychology, primarily fear and greed. And, what motivates people is ultimately those two emotions. And, today what I would call is the greed phase of the market cycle.

UK: What should Canadian investors do with their capital at this stage?

AD: Well, in the book I said if nothing has happened by the end of 2017, that I would be extremely surprised that we have gone this long without a market correction. And that’s one thing about the markets, we never know. But, historically after I have done a bit more research since the book has been written, I now understand that the period between 1921 and 1929 which was the depression, the great crash, the market was able to from trough to peak realized a gain of 400%. And, we just breached 300%.

In fact they’re still potentially a bit more what I would call euphoria before we could see a correction but we’re at the point now where things are very dangerous. You know psychology playing such a role, people believe in fear of missing out (FOMO) and more and more people are in the markets, or want to get in the markets and that’s typically from my experience of living through two other market corrections professionally and three or four just being sort of a novice investor, that it always is the same at the top of every market. And, this is a very familiar territory for me, it reminds me a lot of 2000 and technology bubble. I could say that to give you some analogies, I would say that technology stocks are very similar to today’s either crypto currencies or marijuana stocks. They are just a euphoria that everybody wants it. And, that typically means we are probably close to the end.

UK: I will confess, I have bought some crypto myself. You have spent 25 + years guiding Canadian investors to financial success. How were you able to convince clients to stick with you during a bear market? Have you lost clients during a market crash?

AD: To be honest with you, we lose clients, every advisors loses clients both in the bad markets and in good markets. I recently did lose a client because they were not getting returns they were expecting. If you take a look at the market today, that’s the problem. When people see the markets, especially in the US now getting 25% annual rate of return and their portfolios are up maybe 6, 7, 8%, there’s a feeling that they’re missing out and that causes people to get frustrated and that causes people to move. So, that’s the dilemma. People want the returns but taking more risk in your portfolio to achieve those returns is ultimately, the inevitable sort of the downfall of when the crushing comes. It happens very fast, very violent and people lose a lot of money very quickly.

UK: Like you said, you have experienced two market corrections in your professional career, 2000-2002 and 2007-2009. What lessons have you gained from the two market corrections? I ask because I have never experienced a bear market as I started investing only in 2010. I will be honest, I am low-key excited for a market crash.

AD: One of the reasons why I wrote the book is because I was investing because I believed in what I was told and learned from all of the financial models and all of the financial courses that I had taken to become an advisor that is the markets cannot be timed, buy and hold, you are in it for the long term. Over the long term, you’ll do fine and I was investing my money exactly the same as I was investing my client’s money. I was not trying to time the market so I was watching the asset allocation. I would say I had a balanced portfolio, and I experienced 2000 and I said, Oh that’s what I get, I am a long term investor just like my clients and recovered of course with everyone else and got to 2007 and of course, had the same experience again. And, in 2009 that’s when I started to think about I believe there is another way. I believe there is another strategy, another formula and if you take a look at, for instance, at William J O’Neil’s book that I told you, there is phenomenal charts in there that show that companies have earned rates of return of 800, 900, a thousand percent, two thousand percent and once you start to really examine those charts that he has in that book, those companies with those return were not made from this point of the market cycle. If you take a look at where those charts started and where they ended and they all started at the beginning of a market cycle. He goes back to the 1950’s, 60’s 70’s right up to almost present day because they keep on revising the book and if you take a look at any chart in there, all of the serious gains are made from the bottom of the market cycle.

UK: In 2000, right before the technology meltdown occurred, the S & P 500 index level was at 1450. Seven years later (2007), right before the financial crisis, the S & P level touched 1500. This produced a return of 3% for the “buy and hold” investor. However, from 2007 to 2017, a “buy and hold” investor produced a total return of 8.5%.

AD: Yes, compounded.

UK: Yes. I am aware you are not the biggest fan of “buy and hold”. But, 8.5% is a pretty good return for an average investor. What are you thoughts?

AD: That’s a very valid point but we have yet to see a market correction yet. For the people who are not selling at some point in the very near future, they will go down in that cycle and that will diminish much of their returns. And that’s why I say it is time to take at least a portion of your profits off the table. We are very long in the market cycle here and if you continue to be all in, you will suffer the ramifications of something pretty dramatic happening going forward.

UK: In your book, you talk about the housing bubble. The price of real estate in Canada is overvalued especially in cities like Toronto and Vancouver. What advice would you give to Canadian Millennials, let’s say 24 to 37 year olds who are looking to buy a house?

AD: Here’s the thing, I can give people all the advice in the world but people are going to make their own decisions and they need to make their own mistakes. I just hope like me they don’t make too big mistakes that they can’t recover from. People need to make their own mistakes. To answer your question, I have three nieces that have all bought houses in a relatively short period of time

UK: They are in that age group, 24 – 37.

AD: Exactly. I tried to say to them maybe perhaps waiting would be a good idea because if something were to happen, they might be able to get a better price down the road. None of them listened to me but I understand people have to make their own decisions in the end and they will inevitably find out through the course of time that you can live through anything you know we can go, it’s amazing human nature and human beings can suffer some very incredible sorts of shock to their life but we always come back. We can always recover from them. Unfortunately, we learn by making those mistakes.

UK: TFSA (Tax Free Savings Account). I love TFSA. It is an amazing investment vehicle for Canadians as it allows investors to shelter gains tax free. But, we do know that the government will continue to lose more revenue each year. Please forgive me if I sound like a pessimist but do you see this program being cancelled in the future?

AD: Absolutely. I am not sure if I mentioned it in the book or not but the people or one of the person that created TFSA actually said that this is a bad idea and we should sort of and try and curve this back a little because of the loss revenue as you mentioned already. So, I guess at the start you know having people shelter 20, 30, 40 thousand dollars was not a big deal that the government could forgo those tax free capital gains. However, as we go through a number, really time in the compounding wealth effect then these, there are some people with $400,000 $500,000 TFSA and now, the government realizes that they are not able to capture the gains on theses type of accounts. So, yes they have been allowing contributions to accumulate year after year, I think that’s probably the first thing that gets cancelled. So, if you haven’t made the contribution already, you will not be grandfathered. I think that’s probably the first thing that they will probably start to do if they start to take away some of these benefits and the second thing is they’re going to keep the contributions low or take away the whole program.

UK: They did decrease it from 10K to $5500 in 2016.

AD: Yes, exactly.

UK: You recommend 20 stocks for “The Plan” in your book. I don’t remember all 20 but there is RBC, TD, Enbridge, Apple, Starbucks, Nike, Costco, Telus, Canadian Tire, et cetera et cetera. What is your reasoning for choosing these 20 stocks?

AD: Okay. The reason is twofold. One, I wanted to identify companies that have prospered through multiple market cycles if I could find them and most of the all-star team as I call them in my stock selection have survived multiple market cycles. That was the first criteria.

UK: Is it fair to say past performance is no guarantee of future returns.

AD: Yes, absolutely but I am not necessarily talking about performance. I am talking about companies that are able to be in business, that are able to survive even in tough economic conditions. Typically, if you have a track record of being able to do that i.e. a company that has been around for 50 or 100 years, then the likelihood of that company surviving through the next economic downturn is probably pretty good. And, the second reason is that I’ve owned most of these companies in client portfolios a lot of the last 25 years of my profession.

UK: If any of my readers are interested in seeing you, what are your consultation fees? How much do you charge for an hour?

AD: Okay, I am a full service investment advisor. I make money by people allowing me to manage their assets. So, I would say majority of my clients right now are predominantly in cash. So, in fact I am not earning any money just like my clients. My clients, I am giving them a rate of return on the cash they are holding in their portfolios exactly where my portfolio is positioned. I don’t expect my clients to pay me money in order to earn cash or not be invested in the market. So, I am forgoing my fees today in order to preserve the capital of my clients. It is very challenging for me to do that today because of the psychology of the fear of missing out but I will ultimately be right and that’s when I think, I will be more familiar to people when the ultimate sort of what I think is going to happen, starts to happen. That’s when I will become a more popular person than I am today.

UK: Correct. But, again if any of my readers wants to be a new client of yours, how would they proceed?

AD: They can simply read my book or just go to my website www.thenextbullmarket.com and they can just connect with me from my website.

UK: Alan, I know you blog as well. How many times do you write in a week?

AD: That depends on my schedule. If I am busy doing things like I am right now with the library and some other things I am doing, I don’t get a chance or the opportunity to write but I have got some extremely exciting things happening that I am very excited about and of course as the market does what I think is going to do, that will give me the opportunity to start getting a lot more you know a lot more sort of out there in terms of my understanding of what’s happening and why I think its happening. So, I am going to be more active than I have been. Let me tell you, for instance, one thing that I am excited about. There is a great book called, The Alchemy of Finance, written by George Soros. He is a very popular guy and everyone knows him. He is a billionaire, hedge fund manager. And, in the middle of that book, we get golden nuggets form everything, everything we read, whether we like it or not, there’s always a golden nugget to get and in the middle of that book, there is a little portion that talks about his real time trade that he did, that made him a phenomenal amount of money and I am planning to do the same thing. So, when the market corrects, I am going to be doing a real time analysis of when I am getting into the market, what the stock prices are and going to be sort of dynamically doing that whole process and putting it in a blog or an email or something to let people know exactly sort of what’s happening.

UK: What is the book called again?

AD: The Alchemy of Finance. It is not a fun read but there are golden nuggets in everything we get.

UK: What is your writing practice like? Do you prefer writing in the morning, daytime or night time?

AD: Hahah. It’s called inspiration I think. There were times when I was writing the book, I had a bit of a block and I had to sort of take a couple of days off and just sort of think about it. And, then there were days where it just seems to flow naturally. But, I tend to do my best work in the morning because in the afternoon, I am sort of a little sluggish.

UK: Lastly, what are bad recommendations you hear in your profession or area of expertise? What advice should Canadians ignore?

AD: About investment advice?

UK: Ya.

AD: Oh, I am going to ruffle a few feathers here. This industry is predicated on some things that a lot of people don’t understand or don’t realize or know. One of them is that assets must be invested for fees to be generated. So, a lot of people in this business are paid to be bullish. Even if they think themselves that the markets are very dangerous, they are not going to say it because they don’t want people to pull assets from their firms. Buy and hold, you are in it for the long term. Ya, if you are a 30 year old, that’s right but most of my clients are pre-retired or retired and they are not in it for the long term. There is significant risk to them if they take a big hit in their portfolio that they will run out of money. And, I had conversations with clients in the past about them, after market correction and losing 20, 30, 40% and it’s not a fun experience. That’s the part of the job that no advisor enjoys. And, it puts a lot of stress on advisors when we go through corrections because we feel personally responsible for clients’ money as well and I don’t like having those conversations. Hence, why I don’t have my clients in a lot of risk assets right now.

UK: Perfect. Thank you Alan for your time.

AD: My pleasure.

You can follow Alan on twitter here.

Can you interview Hilliard Macbeth and inquire about his thoughts on real estate in 2018? He’s the author of When the Bubble Bursts.

Keep up the great work!

Thank you. Yes, will do my best to get him as well. I have not read his book. How did you find it?

Thank you for doing these short and concise interviews on personal finance authors. It helps to get a good summary and provides further context around the author’s mindset and philosophy behind their books. Keep interviewing!

Thank you, already got a couple of personal finance authors lined up for interviews. Stay tuned 🙂